US Unemployment Rate Unexpectedly Dropped to 4.2% in June

Why did America's jobless rate dip with slower job creation?

By: Andrew Moran | July 6, 2026 | 593 Words

(Photo by Spencer Platt/Getty Images)

As summer temperatures continue to rise, the already hot US labor market could be starting to cool off. The highly anticipated June jobs report was released on July 2, and the headline reading of 57,000 new jobs came in below economists’ expectations. But America’s unemployment rate last month surprised market watchers, as well, which was both good and bad.

Inside the Unemployment Rate

June’s unemployment rate came in at 4.2%, according to the Bureau of Labor Statistics. This was down from 4.3% in May and lower than the consensus forecast.

The unemployment rate is a core labor market indicator calculated from the Current Population Survey, a monthly household survey conducted by the federal agency.

It represents the share of the labor force that is unemployed and counts those aged 16 or older who do not have a job, are available to work, and have actively searched for work in the past four weeks. On the other hand, the measure excludes discouraged workers who want a job but are no longer looking for employment.

So, if the economy added fewer jobs than expected, why did the widely watched metric come down? Economists examine the break-even employment growth rate.

The break-even rate is the number of new jobs necessary to keep the jobless rate low. It considers immigration, population growth, and labor-force participation. Due to President Donald Trump’s immigration policy changes and fewer workers staying in the workforce, the unemployment rate has been quite low. This was displayed in the June jobs data.

The break-even rate is the number of new jobs necessary to keep the jobless rate low. It considers immigration, population growth, and labor-force participation. Due to President Donald Trump’s immigration policy changes and fewer workers staying in the workforce, the unemployment rate has been quite low. This was displayed in the June jobs data.

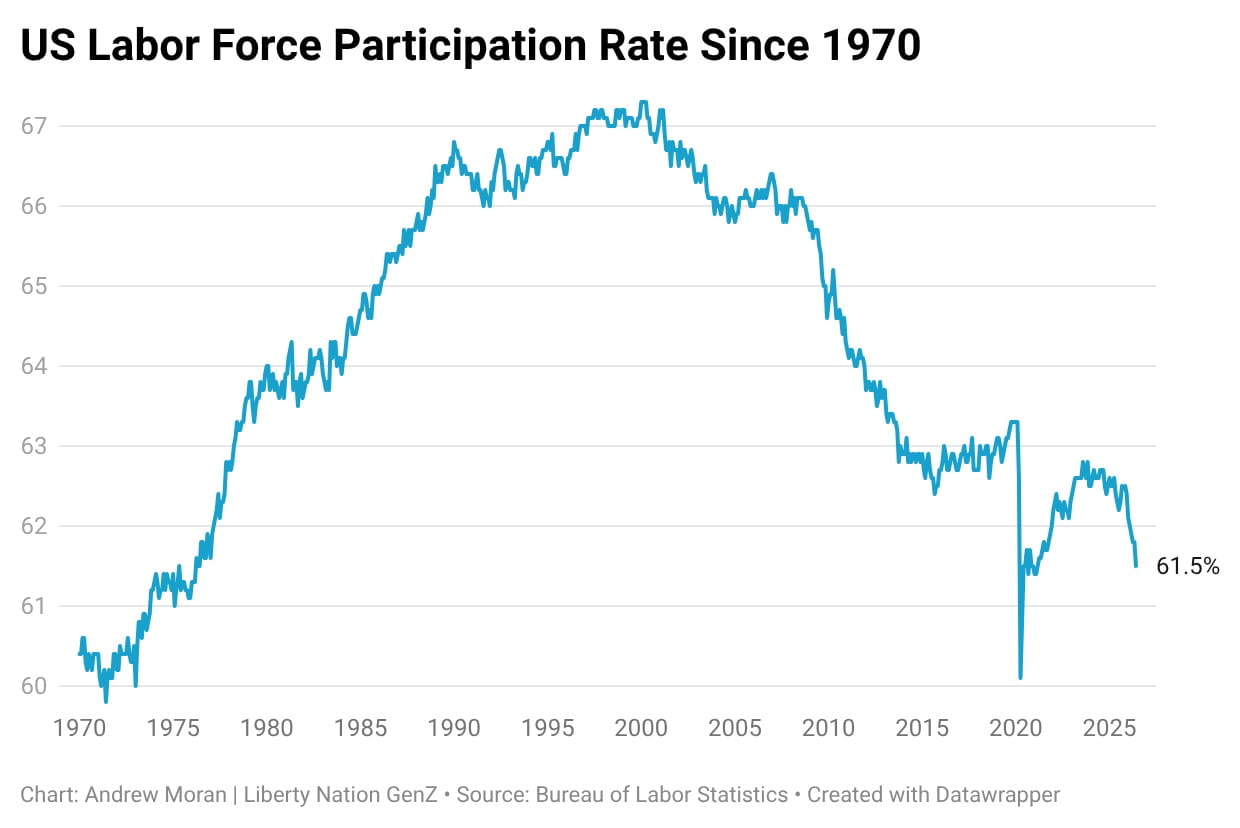

The labor force participation rate declined by 0.3% to 61.5%, the lowest level since March 2021 (excluding the pandemic, it is the lowest since 1976). The percentage drop was fueled by 720,000 individuals leaving the labor force.

Because the break-even rate is close to zero, it could stay around 4% for a long time, and this could have implications for the Federal Reserve’s policy decision-making.

What This Means for the Fed

Decades ago, Congress assigned the Federal Reserve a dual mandate: price stability and maximum employment. Put simply, the US central bank must deliver low inflation and low unemployment.

Over the past year, both mandates were simultaneously under threat. Recent employment data, however, suggested that inflation has become a greater risk than the labor market.

Based on recent commentary from new Fed Chairman Kevin Warsh, the institution could be squarely focused on inflation figures rather than job figures.

Based on recent commentary from new Fed Chairman Kevin Warsh, the institution could be squarely focused on inflation figures rather than job figures.

“Compared with our long-run breakeven rate of around 25,000 to 40,000 jobs per month, June’s jobs report still suggests the labor market remains strong, suggesting that the Federal Reserve will focus on containing inflation rather than maintaining maximum sustainable employment,” Joseph Brusuelas, chief economist at RSM, said in a July 2 research note.

Investors still believe the Fed will raise interest rates this year, but the odds could decrease if price pressures continue to cool now that global energy markets are stabilizing.

Hiring Momentum

Various labor market indicators suggest a rebound in employment conditions following two months of volatility at the start of the year. A severe winter storm had essentially paralyzed the broader economic landscape. Since March, however, the situation has improved: The private sector is expanding payrolls, companies are firing fewer employees, and nominal (non-inflation-adjusted) wage growth remains robust.

With the unemployment rate the main barometer for financial markets and policymakers, the labor market could be close to full employment.

- The June jobs report showed lower than expected job growth – but also lower than expected unemployment.

- The Federal Reserve has two mandates: Deliver low inflation and low unemployment.

- 2026 got off to a rough start, but now it seems employment is improving.